You receive your payslip and the take-home figure is significantly lower than your gross salary. Where did it all go? This guide explains every line on an Irish payslip — what each deduction is, how it is calculated, and whether yours looks correct. Includes worked examples for a Staff Nurse, a Grade III Clerical Officer, and a Healthcare Assistant.

What Is a Payslip?

A payslip is a written statement from your employer showing your gross pay (before deductions), all deductions made, and your net pay (take-home). In Ireland, employers are legally required to provide a payslip for every pay period under the Payment of Wages Act 1991.

Your payslip may be:

- A paper slip handed to you or posted

- A digital/online payslip accessed through your employer’s HR portal (most HSE staff access payslips through the HSE’s HR system)

- Emailed as a PDF

Regardless of format, it must contain the same information.

The Anatomy of an Irish Payslip

A standard Irish payslip has three main sections:

- Earnings — what you earned before any deductions

- Deductions — tax, PRSI, USC, pension, and other items taken off

- Net Pay — what you actually receive

Let’s look at each section in detail.

Section 1: Earnings (Gross Pay)

Basic Salary / Basic Pay

Your contractual pay for the period — the amount you would earn before deductions if you worked your standard hours. This is the figure your pay scale refers to.

Overtime / Premium Pay

If you worked overtime or unsocial hours (nights, weekends, public holidays), these payments appear separately. For HSE clinical staff, these can be significant additions to basic pay.

Common premium line items on HSE payslips:

- Night Duty Premium — additional pay for working night shifts

- Weekend Premium — Saturday/Sunday allowances

- Public Holiday Premium — enhanced rate for working bank holidays

- On-Call Allowance — Category A/B/C on-call payments (NCHD and some nursing grades)

Allowances

Job-specific additional payments — for example:

- Rural Practice Allowance (PHN, GPs)

- Clinical Nurse Specialist Allowance

- Acting Up Allowance — if you are temporarily covering a higher grade

Total Gross Pay

The sum of basic salary plus all overtime, premiums, and allowances. This is the number from which all deductions are calculated.

Section 2: Deductions Explained

1. PAYE (Pay As You Earn) — Income Tax

PAYE is income tax, collected by your employer and remitted to Revenue on your behalf.

How PAYE is Calculated in Ireland (2026)

Ireland uses a two-rate tax system:

| Income Band (Single Person, 2026) | Tax Rate |

|---|---|

| Up to €44,000 per year | 20% (Standard Rate) |

| Above €44,000 per year | 40% (Higher Rate) |

Married couples / civil partners have a higher standard rate band — up to €53,000 if one spouse earns all the income, or up to €88,000 combined for dual-income couples.

Tax Credits Reduce What You Pay

Your tax credits are subtracted from the gross tax calculated above. Tax credits are not deductions from income — they are direct reductions in the tax bill itself.

Standard tax credits for an employee (2026):

| Tax Credit | Annual Amount (€) |

|---|---|

| Personal Tax Credit | 2,000 |

| Employee (PAYE) Tax Credit | 2,000 |

| Total (standard) | 4,000 |

Additional credits you may be entitled to:

- Home Carer Credit — if you care for a dependent person

- Single Person Child Carer Credit — for lone parents

- Rent Tax Credit — if you rent privately (€750/year for single persons)

- Medical Expenses — relief at 20% on qualifying health expenses

- Pension contributions — contribute to a private pension? Tax relief applies

Your personal tax credit certificate (issued by Revenue) tells your employer exactly which credits you are entitled to. It is crucial that this is correct — check yours on Revenue’s myAccount portal.

2. USC (Universal Social Charge)

USC is a tax on gross income. Unlike PAYE, there are no credits against USC — it is applied directly to your earnings.

USC Rates 2026

| Income Band | USC Rate |

|---|---|

| First €12,012 | 0.5% |

| €12,013 – €25,760 | 2% |

| €25,761 – €70,044 | 4% |

| Above €70,044 | 8% |

Medical card holders and people earning under €13,000 per year pay a reduced USC rate of 0.5% on all income. Always inform your employer if you hold a medical card — it affects your USC calculation.

USC is applied to most sources of income including wages, overtime, and rental income. Pension contributions from your employer are not subject to USC.

3. PRSI (Pay Related Social Insurance)

PRSI funds your entitlement to social welfare benefits — Jobseeker’s Benefit, Illness Benefit, Maternity Benefit, State Pension, and others.

Employee PRSI Rate 2026

Most employees (including all HSE staff) pay Class A PRSI:

| Detail | Rate |

|---|---|

| Employee PRSI rate (2026) | 4.2% |

| Applied to | Gross pay above €352/week (€18,304/year) |

PRSI rates have been increasing incrementally since October 2024 under a government plan to fund pension reform. The rate is scheduled to continue increasing by 0.1% annually through the late 2020s.

Your employer also pays PRSI on your behalf — at a higher rate (approximately 11.15%). This does not appear on your payslip as a deduction because it is an employer cost, not a deduction from your wages.

4. Pension Contributions

If you are a member of a pension scheme (all HSE employees are), your pension contribution is deducted from gross pay before tax in some cases, or from net pay.

HSE Pension Contributions 2026

Single Public Service Pension Scheme (for employees who joined the public service after 1 January 2013):

| Contribution Type | Rate |

|---|---|

| Main pension contribution | 3.5% of gross salary |

| Spouse’s and children’s pension | 1.5% of gross salary |

| Total employee contribution | 5% of gross salary |

Pre-2013 “legacy” scheme (for employees who joined before 1 January 2013):

- Rates vary by scheme (typically 5–6.5% of salary plus 1.5% for spouse’s pension)

Good news: Pension contributions made to an occupational pension scheme attract full income tax relief — they reduce your taxable income before PAYE is applied. This means you do not pay 20% or 40% tax on the portion of your salary that goes to your pension.

However, USC and PRSI are still deducted on gross salary before pension — pension contributions do not reduce your USC or PRSI bill.

5. Other Common Deductions

| Deduction | Description |

|---|---|

| Union dues | If you are a member of SIPTU, Forsa, INMO, IMO — subscription deducted at source |

| VHI / Laya / Irish Life Health | Health insurance premium (if arranged through employer) |

| Bike to Work | Salary sacrifice scheme — repaid from gross pay over 12 months |

| Tax Saver Commuter Ticket | Monthly commuter ticket scheme — deducted from gross pay |

| Cycle to Work Loan repayment | If you took a loan for a bike through the HSE credit union scheme |

| HSE Credit Union | Weekly/monthly savings or loan repayment |

| Season ticket loan | Rail or bus season ticket repaid over 12 months |

Section 3: Net Pay (Take-Home Pay)

Net Pay = Total Gross Earnings − All Deductions

This is the amount deposited to your bank account or paid by cheque. It is also called “take-home pay.”

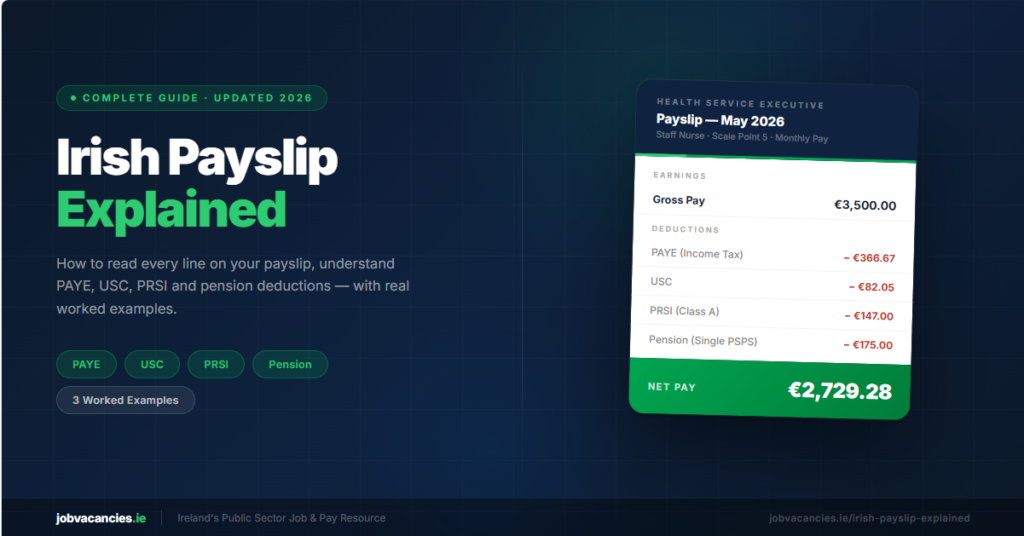

Worked Example 1: Staff Nurse on €42,000 Gross (Annual)

Single person, no dependants, Single PSPS pension, no other deductions

Monthly Gross Salary: €3,500

| Deduction | Monthly (€) | Annual (€) |

|---|---|---|

| PAYE (20% on €42k, less €4,000 credits) | ~367 | ~4,400 |

| USC | ~82 | ~985 |

| PRSI (4.2%) | ~147 | ~1,764 |

| Pension (5% Single PSPS) | ~175 | ~2,100 |

| Total Deductions | ~771 | ~9,249 |

| Net Monthly Take-Home | ~€2,729 | ~€32,751 |

Effective tax rate: approximately 22% of gross pay

Total deductions as % of gross: approximately 22%

This example assumes standard tax credits only. A nurse in a pension scheme from before 2013, with additional allowances or working significant overtime, will have a different payslip.

Worked Example 2: Grade III Clerical Officer on €30,000 Gross (Annual)

Single person, no dependants, Single PSPS pension

Monthly Gross Salary: €2,500

| Deduction | Monthly (€) | Annual (€) |

|---|---|---|

| PAYE (20% on €30k, less €4,000 credits) | ~167 | ~2,000 |

| USC | ~42 | ~505 |

| PRSI (4.2%) | ~105 | ~1,260 |

| Pension (5% Single PSPS) | ~125 | ~1,500 |

| Total Deductions | ~439 | ~5,265 |

| Net Monthly Take-Home | ~€2,061 | ~€24,735 |

Effective tax rate: approximately 17% of gross pay

Percentage kept from gross salary: approximately 82%

Worked Example 3: Healthcare Assistant on €33,500 Gross (Annual)

Single person, no dependants, Single PSPS pension

Monthly Gross Salary: €2,792

| Deduction | Monthly (€) | Annual (€) |

|---|---|---|

| PAYE (20% on €33.5k, less €4,000 credits) | ~192 | ~2,300 |

| USC | ~54 | ~645 |

| PRSI (4.2%) | ~117 | ~1,407 |

| Pension (5% Single PSPS) | ~140 | ~1,675 |

| Total Deductions | ~503 | ~6,027 |

| Net Monthly Take-Home | ~€2,289 | ~€27,473 |

Effective tax rate: approximately 18% of gross pay

All worked examples are illustrative approximations for a single person with standard tax credits only. Your actual payslip will vary based on your specific tax credits, credits from Revenue, additional allowances, overtime, and pension scheme. Use Revenue’s online tax calculator at revenue.ie for a precise calculation.

Why Is My Take-Home Pay Less Than I Expected?

This is the most common payslip question. Here are the most frequent reasons:

1. You’re Comparing Net to Gross

The salary advertised in a job offer is almost always gross — before any tax or deductions. Net pay for a salary of €42,000 can be as low as €32,000 after tax, USC, PRSI, and pension. This is normal.

2. Your Tax Credits Aren’t Set Up Correctly

If your employer has not received your Tax Credit Certificate from Revenue, they must apply Emergency Tax — a much higher rate. Signs of emergency tax:

- The tax band on your payslip is zero or very low

- PAYE deductions seem very high from your first payslip

- You see “Emergency” or “Week 1/Month 1” on your payslip

Fix: Log into Revenue’s myAccount at revenue.ie and ensure your new employer is listed and has your up-to-date credits.

3. You Recently Had a Pay Rise or Bonus

Pay rises and bonuses push your income higher. If a bonus pushes you above the standard rate band (€44,000 for single person), part of it is taxed at 40%.

4. You Have a Pension Deduction for the First Time

Starting pension contributions reduces take-home pay immediately. Remember — this money is not lost, it is being saved for your retirement with tax relief attached.

5. You Changed Jobs Mid-Year

If you moved jobs during the year, your new employer may not yet have all your year-to-date tax information. This can result in too much or too little PAYE being deducted until your P45 (or electronic information) is transferred.

6. A Previous Underpayment Is Being Recovered

If Revenue reassesses your tax and finds you owe tax from a previous period, they may instruct your employer to collect it through a reduced tax credit. This appears as lower credits and higher PAYE on your payslip.

How to Check If Your Payslip Is Correct

Use this checklist to verify your payslip each month:

Step 1: Check Your Gross Pay

- Does it match your contract salary (divided by 12 for monthly pay)?

- Are all overtime, allowances, and premium payments you expect actually showing?

- Are there any unexpected additions?

Step 2: Verify Your Tax Credits

- Log into myAccount on revenue.ie

- Check your current Tax Credit Certificate — does it show the correct employer?

- Are all credits you’re entitled to (personal, PAYE, rent, etc.) listed?

- Does the “Annual Tax Credits” figure on your payslip match?

Step 3: Check the PAYE Calculation

- Take your gross pay and apply 20% (assuming income under €44,000 for single)

- Subtract your monthly tax credits (annual credits ÷ 12)

- The result should approximately match the PAYE on your payslip

Step 4: Check USC

- USC is a straightforward percentage of gross — refer to the rate bands above

- If your USC seems very high, check your payslip for an emergency USC rate

Step 5: Check PRSI

- Should be 4.2% of gross pay (2026 rate for Class A)

- If you earn under €352/week you may be exempt — check with payroll

Step 6: Check Pension Deduction

- Should be 5% of gross for Single PSPS members (or your scheme’s rate)

- If you see no pension deduction after your probation period, check with HR

Step 7: Check Other Deductions

- Do you recognise every deduction listed?

- If something appears that you didn’t authorise (union membership, health insurance, loan repayments), contact payroll to query it

What to Do If Your Payslip Is Wrong

For Tax Issues (wrong PAYE, credits missing)

- Contact Revenue via myAccount or by phone (01 738 3636)

- Update your tax credits and ensure your employer has your current certificate

- Revenue can also review and refund overpaid tax at year end

For Payroll Errors (wrong salary, missing overtime, incorrect deductions)

- Contact your payroll department or HR Business Partner in writing (email creates a record)

- Provide the specific payslip date and the specific error

- Underpayments must be corrected promptly — your employer has a legal obligation under the Payment of Wages Act

For Pension Queries

- Contact your HSE HR Pensions section or the Single PSPS administrator (DPER)

- Pension statements are issued annually — compare these to your payslip deductions

Understanding Your Payslip Year-to-Date (YTD) Figures

Most payslips include a Year-to-Date (YTD) column showing the accumulated total of all earnings and deductions from January 1st to the current period. This is useful for:

- Verifying your annual tax position

- Estimating your end-of-year tax review outcome

- Checking you are on track with pension contributions

At the end of the tax year (December), your YTD figures should match what Revenue has on record for you. Revenue’s myAccount allows you to see your Employment Detail Summary (formerly P60) in January after each tax year closes.

Key Terms on Your Payslip — Glossary

| Term | Meaning |

|---|---|

| Gross Pay | Total earnings before any deductions |

| Net Pay | Take-home pay after all deductions |

| PAYE | Pay As You Earn — income tax |

| USC | Universal Social Charge |

| PRSI | Pay Related Social Insurance |

| Tax Credit | Amount reducing your tax bill directly |

| Standard Rate Band | Income taxed at 20% (€44,000 for single, 2026) |

| Week 1 / Month 1 | Emergency tax basis — credits not applied cumulatively |

| YTD | Year to Date — running total since January 1st |

| Taxable Pay | Gross pay minus any pre-tax deductions (e.g. pension) |

| PRSI Class | The PRSI contribution class you are in (most employees: Class A) |

| LSI | Long Service Increment — top of pay scale |

| Emergency Tax | Higher rate applied when Revenue has no tax credit cert for you |

Frequently Asked Questions

Why is my take-home pay so much less than my salary?

Because your gross salary has several deductions before it reaches you: income tax (PAYE), Universal Social Charge (USC), PRSI, and pension contributions. For an Irish employee, these typically amount to 18–35% of gross pay depending on salary level and personal circumstances.

What percentage of my salary do I keep in Ireland in 2026?

A single person on €30,000 keeps approximately 82% of gross. On €42,000, approximately 78%. On €60,000, approximately 67%. Higher earners keep less due to the 40% tax rate applying above €44,000.

What is USC and is it the same as income tax?

No — USC (Universal Social Charge) is a separate tax from PAYE income tax. You pay both. USC has its own rate bands and cannot be reduced by tax credits. It funds general government expenditure (not specifically social welfare).

Why am I paying emergency tax?

Emergency tax is applied when Revenue has not issued a Tax Credit Certificate to your employer — usually when starting a new job. To fix it, log into Revenue’s myAccount portal, check your employer is listed, and request that your certificate is sent to them. You will get a refund of any overpaid tax.

Are pension contributions taken before or after tax?

Occupational pension contributions (including HSE pension) are taken from gross pay before PAYE is calculated. This means you get tax relief at your marginal rate on contributions — a significant benefit. However, USC and PRSI are still charged on gross salary before pension deduction.

What is the difference between PRSI and a pension contribution?

PRSI builds your entitlement to social welfare benefits (Illness Benefit, Maternity Benefit, State Pension). Your occupational pension contribution goes into a separate pension fund that provides your employer’s pension when you retire. Both appear on your payslip but serve very different purposes.

How do I get a refund if I overpaid tax?

Revenue issues a year-end review (P21 Balancing Statement) after the tax year ends. If you overpaid, you receive a refund — usually processed within a few weeks. You can claim it proactively via myAccount. Common reasons for overpayment include emergency tax, unclaimed credits, or mid-year job changes.

What should I do if overtime is missing from my payslip?

Contact your payroll or HR department in writing, reference the specific dates and hours worked, and ask for the error to be corrected. Under the Payment of Wages Act 1991, underpayments must be addressed promptly.

What does “Week 1 basis” or “Month 1 basis” mean on my payslip?

It means your tax is being calculated without carrying forward year-to-date figures — each period is treated independently. This typically happens at the start of employment or after a tax cert issue. It can lead to higher-than-normal tax. Resolve by contacting Revenue via myAccount.

Useful Links and Tools

- Revenue myAccount — view and manage your tax credits, employer registrations, and tax history: revenue.ie/myaccount

- Revenue Tax Calculator — estimate your net pay: revenue.ie

- myPRSI / MyWelfare — check your PRSI contribution record: mywelfare.ie

- Single Public Service Pension Scheme — information on the post-2013 HSE pension: singlepensionscheme.gov.ie

Related Guides on This Site

- HSE Pay Scales 2026 — Complete Guide

- HSE Pension Scheme — What You Need to Know (coming soon)

- HSE Maternity Leave Policy 2026

- Staff Nurse Salary Ireland 2026

- Healthcare Assistant Salary Ireland 2026

Disclaimer: This guide is for general information purposes only. Tax rates, bands, and credits are based on the 2026 tax year and are subject to change. Your actual take-home pay will depend on your personal tax credits, employment contract, pension scheme, and individual circumstances. Use Revenue’s online calculator at revenue.ie for a precise calculation, and contact your payroll department or a tax advisor if you have a specific query about your payslip.